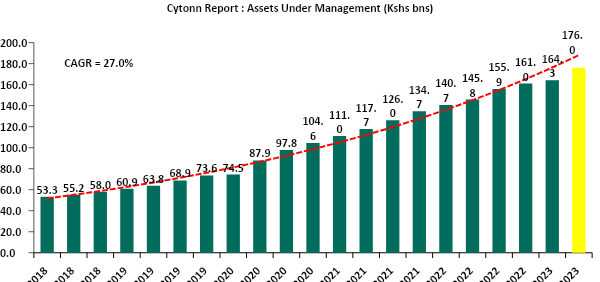

As per the Capital Markets Authority (CMA) Quarterly CIS Report - Q2’2023, the industry’s overall Assets under Management (AUM) registered a significant growth of 7.1% on a quarter on quarter basis to Kshs 176.0 bn as at the end of Q2’2023, from Kshs 164.3 bn recorded in Q1’2023. On a y/y basis, the total AUM increased by 20.7% to Kshs 176.0 bn, from Kshs 145.8 bn as at the end of Q2’2022. Key to note, Assets under Management of the Unit Trust Funds have registered an upward trajectory over the last five years, growing at a 5-year CAGR of 27.0% to Kshs 176.0 bn in Q2’2023, from Kshs 53.3 bn recorded in Q2’2018. The key takes outs from the performance of the Unit Trust Funds include;

-

Assets Under Management:

Source: Capital Markets Authority Quarterly CIS Report

-

Approved Collective Investment Schemes:

According to the Capital Markets Authority, as at the end of Q2’2023, there were 36 Collective Investment Schemes (CISs) in Kenya, up from 34 recorded at the end of FY’2022 and 31 recorded at the end of Q2’2022. Out of the 36 schemes, 27 of them (equivalent to 75.0%) were active while 9 (25.0%) were inactive. The table below outlines the performance of the Collective Investment Schemes comparing Q1’2023 and Q2’2023:

Source: Capital Markets Authority: Quarterly Collective Investments Schemes, Q2’2023

Key take outs from the above table include:

-

Assets Under Management: CIC Unit Trust Scheme remained the largest overall Unit Trust Fund, recording an AUM growth of 4.6%, to Kshs 59.6 bn in Q2’2023, from the AUM of Kshs 57.0 bn recorded in Q1’2023,

-

Growth: In terms of AUM growth, Etica Capital Limited recorded the highest growth of 921.1% with its AUM increasing to Kshs 54.2 mn, from Kshs 5.3 mn in Q1’2023, due to the low base effect. On the other hand, African Alliance Kenya recorded the largest decline with its AUM declining by 18.8% to Kshs 1.3 bn in Q2’2023, from Kshs 1.6 bn in Q1’2023,

-

Market Share: CIC Unit Trust Scheme remained the largest overall Unit Trust with a market share of 33.9%, a decline of 0.8% points, from 34.7% recorded in Q1’2023. The continued decline in market share is an indication of increasing competition as new collective schemes enter the market,

-

New Collective Investment Schemes: Jubilee Unit Trust Scheme and Enwealth Capital Unit Trust, with AUMs of Kshs 359.8 mn, and Kshs 25.5 mn respectively, became active collective investment schemes in the capital market during Q2’2023, taking the total number of active collective schemes to 27, and,

-

9 UTFs remained inactive as at the end of Q2’2023: First Ethical Opportunities Fund, Adam Unit Trust Fund, Masaru Unit Trust Fund, Jaza Unit Trust Fund, Dyer and Blair Unit Trust Scheme, Diaspora Unit Trust Scheme, Standard Investments Bank, Genghis Specialized Fund and Amaka Unit Trust remained inactive as at the end of Q2’2023.

Money Market Funds had the highest average effective annual yield declared, with the Cytonn Money Market Fund having the highest effective annual yield at 11.1% against the industry Q2’2023 average of 9.8%.

Source: Daily Nation, Cytonn Research

-

Comparison against other asset classes

Over the past 5 years, Unit Trust Funds (UTFs) AUM has exhibited positive performance, having grown at a 5-year CAGR of 27.0% to Kshs 176.0 bn in Q2’2023, from Kshs 53.3 bn recorded in Q2’2018. However, the industry is still dwarfed when compared to other deposit taking institutions such as bank deposits, with the entire banking sector deposits coming in at Kshs 5.2 tn as at June 2023 from Kshs 4.8 tn recorded in March 2023. Similarly, the pension industry recorded an increase of 1.9%, to Kshs 1.6 tn as of December 2022 from Kshs 1.5 tn recorded in December 2021. Below is a graph showing the sizes of different saving channels and capital market products in Kenya;

* Data as of December 2022

Source: CMA, RBA, CBK, SASRA Annual Reports and REITs Financial Statements

-

Recommendations

In order to improve our Capital Markets and stimulate UTFs growth, we recommend the following actions:

-

Lower the minimum investment amounts: Currently, the minimum investment for sector specific funds is Kshs 1.0 mn, while that for Development REITS is currently at Kshs 5.0 mn. According to the Kenya National Bureau of Statistics, 87.7% of employees are earning below Kshs 100,000.0 monthly. As such, the high minimum initial and top up investments amounts for investing in sector specific funds deter potential investors. Furthermore, these high amounts disadvantage the majority of retail investors by restricting their options for investments,

-

Open up Trusteeship to Corporate Trustees and Lower Capital Requirement for REIT Trusteeship: Currently, the capital requirement is pegged at Kshs 100.0 mn for REITS trustees in Kenya on top of the requirement that the trustee must be a bank. Lowering the capital to Kshs 10.0 mn would encourage more companies enter the market and provide more options to investors. Similarly, opening trusteeship to Corporate will increase competition leading to better services to investors and overall growth of the UTF industry,

-

Allow for private market instruments to drive Competition: Private market instruments such as private equity, private placements, and private debt are not regulated by the Capital Markets Authority (CMA) in Kenya. Private market instruments can provide alternative sources of capital for businesses, which can help to increase competition and innovation in the market. Additionally, private market instruments often offer higher returns than traditional investment options, which can attract more investors to the market thus fueling growth in the industry

-

Encourage innovation and diversification of UTFs’ investments: Majority of UTFs’ investments are either in fixed income or fixed deposits, highlighting high concentration risks. There is need to encourage fund managers to invest in different sectors of the economy as this will spur diversification of investments such as real estate and private offers. As at 30th June 2023, the total allocation to Fixed deposits and Government securities stood at 44.4% and 42.8% respectively, accounting for 87.2% of the total AUM for unit trust, thus bringing about concentration risk

-

Update regulations: The current Collective Investments Schemes Regulations in Kenya were formulated in 2001 and have not been updated since, despite the dynamic nature of the capital markets worldwide. This has led to the regulations lagging behind. For instance, the regulations do not include provisions for private offers that have grown in importance over the years. The regulations also lack stipulated guidelines on special funds to cater for the sophisticated investors’ interest in regulated alternative investments products. While there are efforts to update the regulations, we note that they remain in progress and are yet to be completed,

-

Allow for sector funds: Under the current capital markets regulations, UTFs are required to diversify. However, one has to seek special dispensation in the form of sector funds such as a financial services fund, a technology fund or a Real Estate Unit Trust Fund. Regulations allowing unit holders to invest in sector funds would go a long way in expanding the scope of unit holders interested in investing. For example, in Kenya, Real Estate continues to play an important role in the economy contributing 10.0% to the GDP as of March 2023 and remains a popular investment option due to the stable returns it delivers and low correlation with traditional investments. However, looking at the various types of Unit trust we have, investments in real estate are conspicuously missing.

-

Incentives: Introduce incentives such as tax benefits or government subsidies for unit trust fund investments, to encourage more people to consider them as part of their investment portfolio, similar to pensions and Education plans. This will be of great importance in encouraging investors to invest in a long time horizon

-

Better disclosure by UTFs: For an investor to make an informed decision they need to be provided with a detailed portfolio holding of the UTFs. Investors need to understand where they moneys are invested so as to be aware of the risk their investments are exposed to. The information should be available to the investors and also to prospective clients

-

Eliminate conflicts of interest in the capital markets governance and allow non-financial institutions to also serve as Trustees: The capital markets regulations should foster a governance structure that is more responsive to both market participants and market growth. In particular, restricting Trustees of Unit Trust Schemes to Banks only limits options, especially given the direct competition between the banking industry and capital markets. Notably, the pension industry has 6 non-bank Trustees yet the capital market only has one non-bank Trustee. Opening up the corporate trustee will bring about a more competitive and predictable trustee environment and consequently bring about more innovation and better services by trustees and growth in capital markets

-

Provide Support to Fund Managers: In our opinion, the regulator, CMA needs to include market stabilization tools as part of the regulations/Act that will help Fund Managers meet fund obligations especially during times of distress like when there are a lot of withdrawals from the funds. We commend and appreciate the regulator’s role in safeguarding investor interests. However, since Fund Managers also play a significant role in the capital markets, the regulator should also protect the reputation of different fund managers in the industry.

For more information, kindly see our topical on Unit Trust Fund Performance, Q2'2023