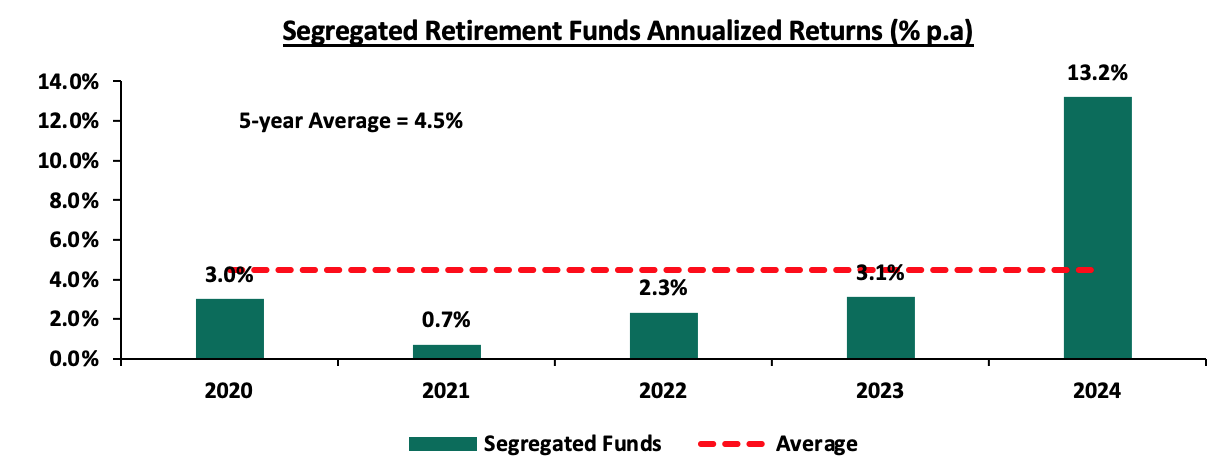

According to the ACTSERV Q4’2024 Pension Schemes Investments Performance Survey, the five-year average return for segregated schemes over the period 2020 to 2024 was 4.5% with the performance fluctuating over the years to a high of 13.2% in Q4’2024 and a low of 0.7% in Q4’2021 reflective of the markets performance. Notably, segregated retirement benefits scheme q/q returns increased to a 13.2% return in Q4’2024, up from the 3.1% gain recorded in Q4’2023. The y/y growth in overall returns was largely driven by the 18.7% points increase in returns from Equities to 15.7% from a loss of 3.0% in Q4’2023 attributable to the increased corporate earnings and attractive valuations as well as the 13.3% gain from fixed income. The performance was however weighed down by the 17.2% points decline in the Offshore returns to 0.8%, from 18.0% in Q4’2023 majorly attributable to the uncertainty about the US general election, China’s weak economic data and the strengthening of the Kenyan Shilling. This week, we shall focus on understanding Retirement Benefits Schemes and look into the quarterly performance and current state of retirement benefits schemes in Kenya with a key focus on Q4’2024;

We have been tracking the performance of Kenya’s Pension schemes with the most recent topical being, Retirement Benefits Schemes Q3’2024 Performance Report, done in December 2024. This week, we shall focus on understanding Retirement Benefits Schemes and looking into the historical and current state of retirement benefits schemes in Kenya with a key focus on 2024 (latest official data) and what can be done going forward. We shall also analyze other asset classes that the schemes can tap into to achieve higher returns. Additionally, we shall look into factors and challenges influencing the growth of the RBSs in Kenya as well as the actionable steps that can be taken to improve the pension industry. We shall do this by looking into the following:

- Introduction to Retirement Benefits Schemes in Kenya,

- Historical and Current State of Retirement Benefits Schemes in Kenya,

- Factors Influencing the Growth of Retirement Benefits Scheme in Kenya,

- Challenges that Have Hindered the Growth of Retirement Benefit Schemes, and,

- Recommendations on Enhancing the Performance of Retirement Benefits Schemes in Kenya;

Section I: Introduction to Retirement Benefits Schemes in Kenya

A retirement benefits scheme is a savings avenue that allows contributing individuals to make regular contributions during their productive years into the scheme and thereafter get income from the scheme upon retirement. There are a number of benefits that accrue to retirement benefits scheme members, including:

- Income Replacement – Retirement savings ensure that your income stream does not stop even when you stop working. After retirement, many people experience a decline in the amount and stability of income relative to their productive years. Retirement savings ensure that this decline is manageable or non-existent and enables you to be able to live the lifestyle you desire even after retirement,

- Compounded and Tax-free interest – Savings in a pension scheme earn compounded interest which means that your money grows faster as the interest earned is reinvested. Additionally, retirement schemes’ investments are tax-exempt meaning that the schemes have more to reinvest,

- Tax-exempt contributions – Pension contributions enjoy a monthly tax relief of up to Kshs 30,000.0 – this lessens the total PAYE deducted from your earnings,

- Avoid old age poverty – By providing an income in retirement, pension schemes ensure that the scheme members do not experience old age poverty where they have to rely on their family, relatives, and friends for survival, and,

- Home Ownership - Savings in a pension scheme can help you achieve your dream of owning a home. This can be done through a mortgage or a direct residential house purchase using your pension savings. A member may assign up to 60.0% of their pension benefits or the market value of the property, whichever is less, to provide a mortgage guarantee. The guarantee may enable the member to acquire immovable property on which a house has been erected, erect a house, add, or carry out repairs to a house, secure financing or waiver, as the case may be, for deposits, stamp duty, valuation fees and legal fees and any other transaction costs required. On the other hand, a pension scheme member may utilize up to 40.0% of their benefits to purchase a residential house directly subject to a maximum allowable amount of Kshs 7.0 mn and the amount they use should not exceed the buying price of the house.

Section II: Historical and the Current State of Retirement Benefits Schemes in Kenya

- Growth of Retirement Benefits Schemes

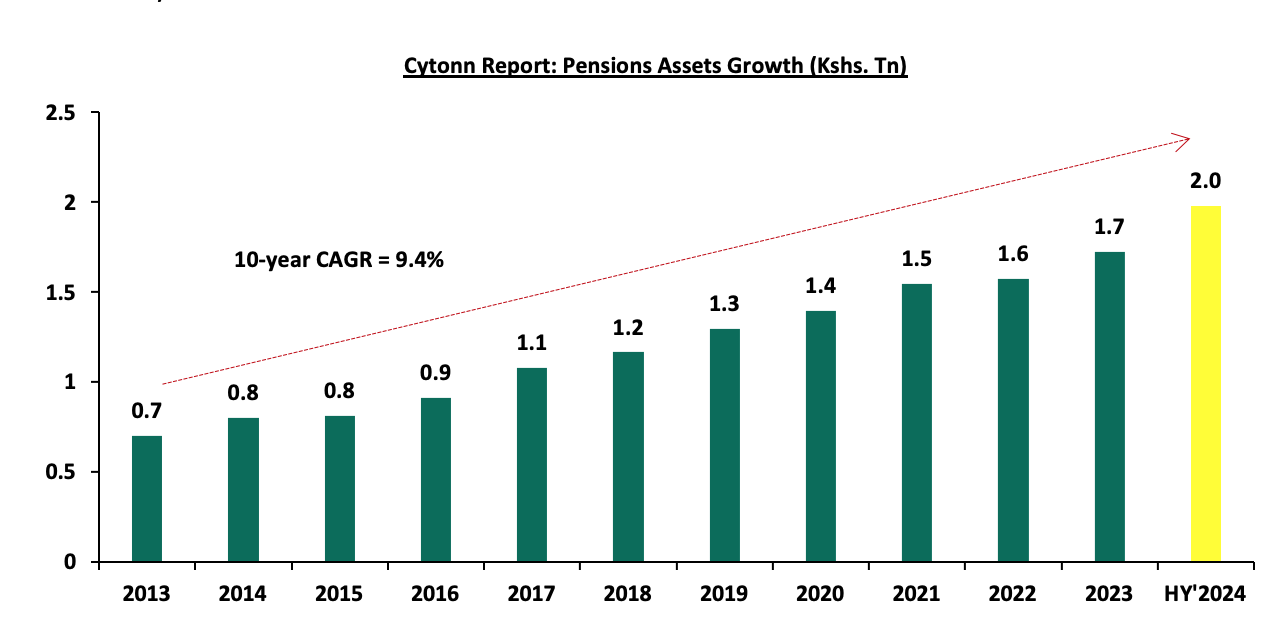

According to the latest Retirement Benefits Authority (RBA) Industry Report for June 2024, assets under management for retirement benefits schemes increased by 14.7% to Kshs 2.0 tn in June 2024 from the Kshs 1.7 tn recorded in December 2023. The growth of the assets is attributed to the improved market and economic conditions during the period as evidenced by improved business conditions, eased inflationary pressures and stability of the exchange rate. Notably, on a year-on -year basis, assets under management increased by 16.1% from the Kshs 1.7 tn recorded in June 2023, partly attributable to the enhanced contributions to the mandatory scheme, NSSF, which began in earnest in February 2023 following the court of appeal ruling. The increase in NSSF contribution limits from February 2025, marking the third phase of implementation under the NSSF Act of 2013, is expected to boost the overall pension sector's assets under management (AUM) by increasing retirement savings.

The graph below shows the growth of Assets under Management of the retirement benefits schemes over the last 10 years:

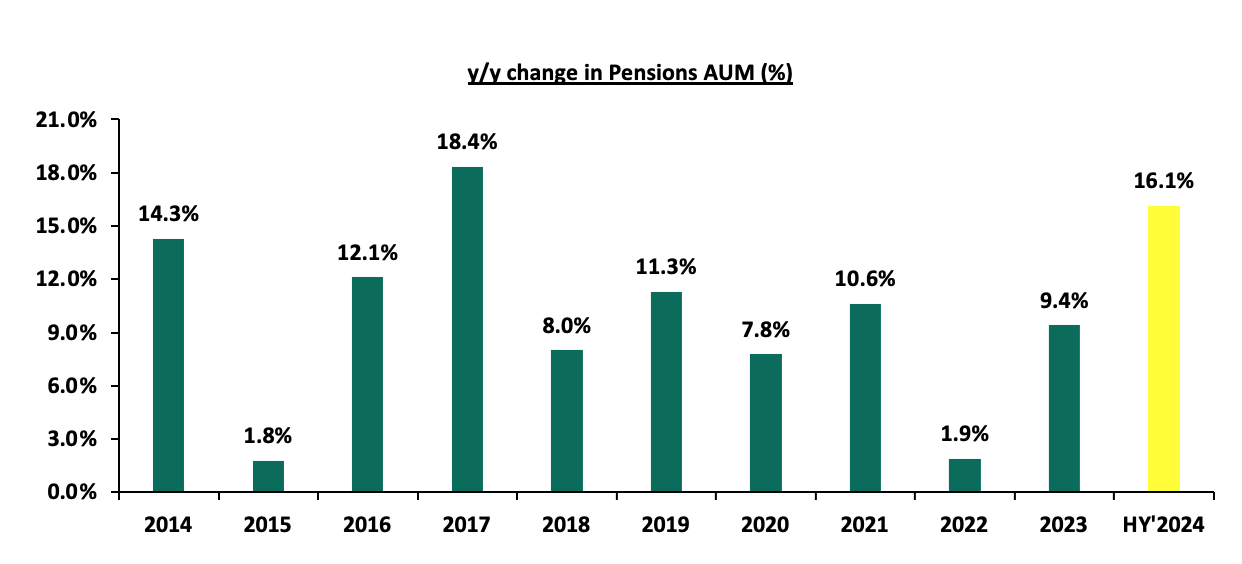

Pensions AUM increased by 14.7% to Kshs 2.0 tn in June 2024 from the Kshs 1.7 tn recorded in December 2023 and by 16.1% on a y/y basis to Kshs 2.0 mn in HY’2024 from Kshs 1.7 mn in HY’2023, which is 6.7% points increase from the 9.4% growth between 2023 and 2022. Additionally, the 9.4% increase in Assets Under Management is 7.5% points increase in growth from the 1.9% growth that was recorded in 2022, demonstrating the significant role that the enhanced NSSF contributions made to the recovery of the industry’s performance following a difficult period in 2022 due to the court ruling that declared revival of NSSF Act No.45 of 2013 unconstitutional. The primary goal of the act was to broaden the NSSF’s benefit coverage, range, and scope as well as improve the adequacy of benefits paid out of the scheme by the Fund amongst others.

The chart below shows the y/y changes in the assets under management for the schemes over the years.

Despite the continued growth, Kenya is characterized by a low saving culture with research by the Federal Reserve Bank indicating that only 14.2% of the adult population in the labor force save for their retirement in Retirement Benefits Schemes (RBSs).

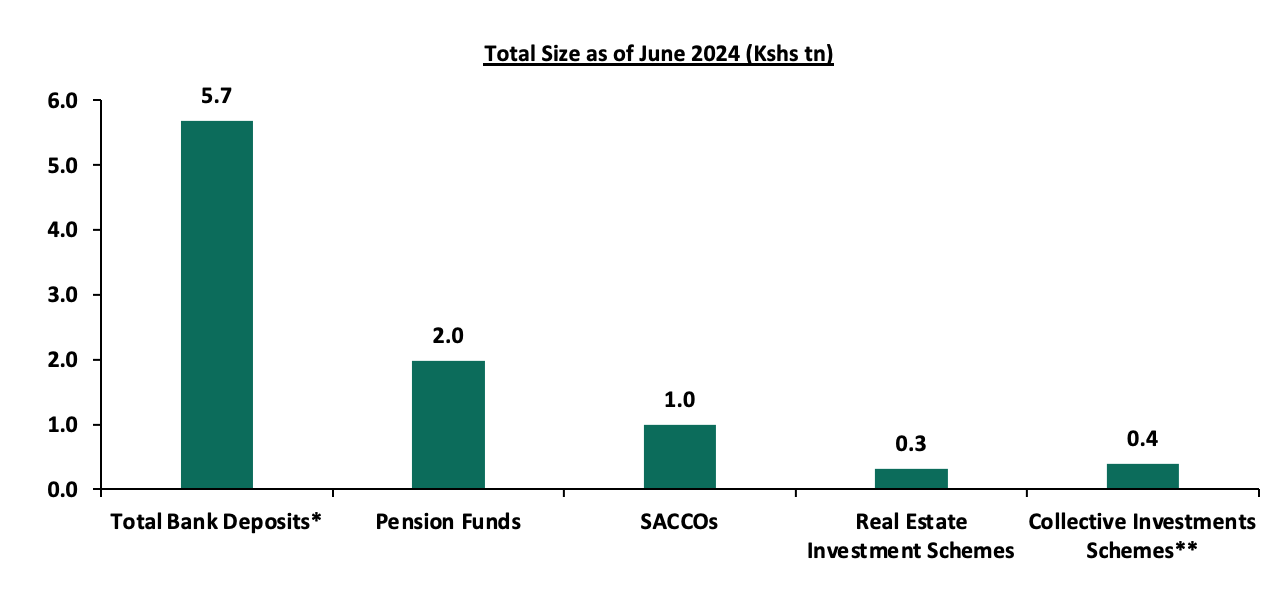

In Kenya, pension funds hold a substantial share of financial assets, consistently growing due to mandatory and voluntary contributions under the National Social Security Fund (NSSF) Act of 2013 regulations. In comparison, bank deposits remain the largest financial pool, reflecting their role as the primary savings vehicle driven by their liquidity, security, and accessibility, though they offer lower returns. Capital markets products, including unit trusts, REITs, are relatively smaller highlighting the nascent stage of capital markets in Kenya, but expanding as investors seek diversification and higher yields. SACCOs play a crucial role in cooperative-based savings and credit access, especially for middle-income earners.

The graph below shows the Assets under Management of Pensions against other Capital Markets products and bank deposits:

Sources: CMA, RBA, SASRA and REIT Financial Statements, *as of Sept 2024, **as of Dec 2024

- Retirement Benefits Schemes Allocations and Various Investment Opportunities

Retirement Benefits Schemes strategically allocate funds across various asset classes available in the market to safeguard members' contributions while striving to generate attractive returns. These schemes have access to a diverse range of investment opportunities, including traditional asset classes such as equities and fixed income securities. Additionally, they can explore alternative investments such as real estate, private equity, infrastructure, and other non-traditional assets, which may offer higher returns and diversification benefits. The choice of investments is guided by the scheme's Investment Policy Statement (IPS), regulatory guidelines, and the need to align with the risk tolerance and long-term goals of the members. As such, the performance of Retirement Benefits Schemes in Kenya depends on a number of factors such as;

- Asset allocation,

- Selection of the best-performing security within a particular asset class,

- Size of the scheme,

- Risk appetite of members and investors, and,

- Investment horizon.

The Retirement Benefits (Forms and Fees) Regulations, 2000 offers investment guidelines for retirement benefit schemes in Kenya in terms of the asset classes to invest in and the limits of exposure to ensure good returns and that members’ funds are hedged against losses. According to RBA’s Regulations, the various schemes through their Trustees should formulate their own Investment Policy Statements (IPS) to Act as a guideline on how much to invest in the asset option and assist the trustees in monitoring and evaluating the performance of the Fund. However, the Investment Policy Statements often vary depending on risk-return profile and expectations mainly determined by factors such as the scheme’s demography and the economic outlook.

The Retirement Benefits Authority (RBA) regulations also emphasize the importance of diversification as a key principle in managing pension funds. By setting limits on exposure to specific asset classes, the regulations mitigate the risks associated with market volatility, ensuring that no single investment disproportionately affects the scheme's overall performance. Trustees are required to regularly review and update their Investment Policy Statements (IPS) to reflect changes in market conditions, economic dynamics, and the evolving needs of the scheme's members. This proactive approach not only aligns the investment strategy with the scheme’s objectives but also enhances accountability and transparency in fund management, safeguarding members’ retirement savings. The table below represents how the retirement benefits schemes have invested their funds in the past:

|

Cytonn Report: Kenyan Pension Funds’ Assets Allocation |

|||||||||||||

|

Asset Class |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

HY’2024 |

Average |

Limit |

|

Government Securities |

31.0% |

29.8% |

38.3% |

36.5% |

39.4% |

42.0% |

44.7% |

45.7% |

45.8% |

47.5% |

51.1% |

41.1% |

90.0% |

|

Immovable Property |

17.0% |

18.5% |

19.5% |

21.0% |

19.7% |

18.5% |

18.0% |

16.4% |

15.8% |

14.0% |

11.9% |

17.3% |

30.0% |

|

Quoted Equities |

26.0% |

23.0% |

17.4% |

19.5% |

17.3% |

17.6% |

15.6% |

16.5% |

13.7% |

8.4% |

8.8% |

16.7% |

70.0% |

|

Guaranteed Funds |

11.0% |

12.2% |

14.2% |

13.2% |

14.4% |

15.5% |

16.5% |

16.8% |

18.9% |

20.8% |

20.5% |

15.8% |

100.0% |

|

Fixed Deposits |

5.0% |

6.8% |

2.7% |

3.0% |

3.1% |

3.0% |

2.8% |

1.8% |

2.7% |

4.8% |

2.7% |

3.5% |

30.0% |

|

Listed Corporate Bonds |

6.0% |

5.9% |

5.1% |

3.9% |

3.5% |

1.4% |

0.4% |

0.4% |

0.5% |

0.4% |

0.4% |

2.5% |

20.0% |

|

Offshore |

2.0% |

0.9% |

0.8% |

1.2% |

1.1% |

0.5% |

0.8% |

1.3% |

0.9% |

1.6% |

2.0% |

1.2% |

15.0% |

|

Cash |

1.0% |

1.4% |

1.4% |

1.2% |

1.1% |

1.2% |

0.9% |

0.6% |

1.1% |

1.5% |

1.2% |

1.1% |

5.0% |

|

Unquoted Equities |

1.0% |

0.4% |

0.4% |

0.4% |

0.3% |

0.3% |

0.2% |

0.2% |

0.3% |

0.2% |

0.2% |

0.4% |

5.0% |

|

REITs |

0.0% |

0.0% |

0.1% |

0.1% |

0.1% |

0.0% |

0.0% |

0.0% |

0.0% |

0.6% |

0.6% |

0.1% |

30.0% |

|

Private Equity |

0.0% |

0.0% |

0.0% |

0.0% |

0.1% |

0.1% |

0.1% |

0.2% |

0.2% |

0.3% |

0.4% |

0.1% |

10.0% |

|

Others e.g. unlisted commercial papers |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.1% |

0.2% |

- |

0.0% |

0.0% |

10.0% |

|

Commercial Paper, non-listed bonds by private companies |

- |

- |

- |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.2% |

0.0% |

10.0% |

|

Total |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

Source: Retirement Benefits Authority

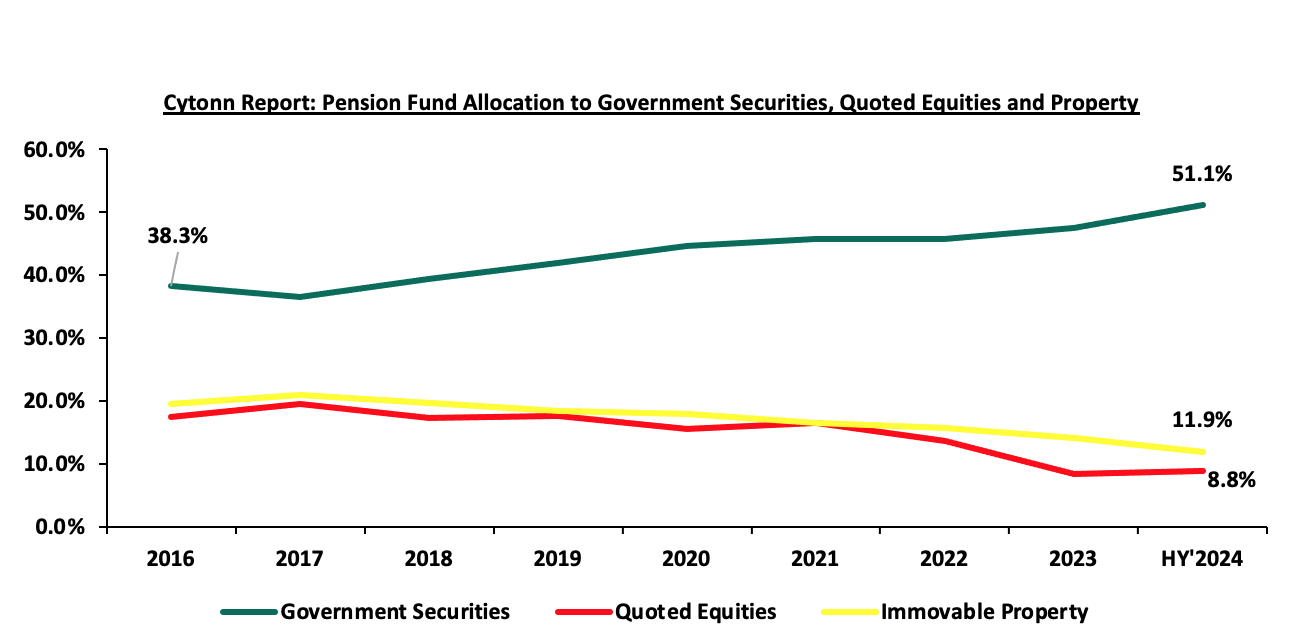

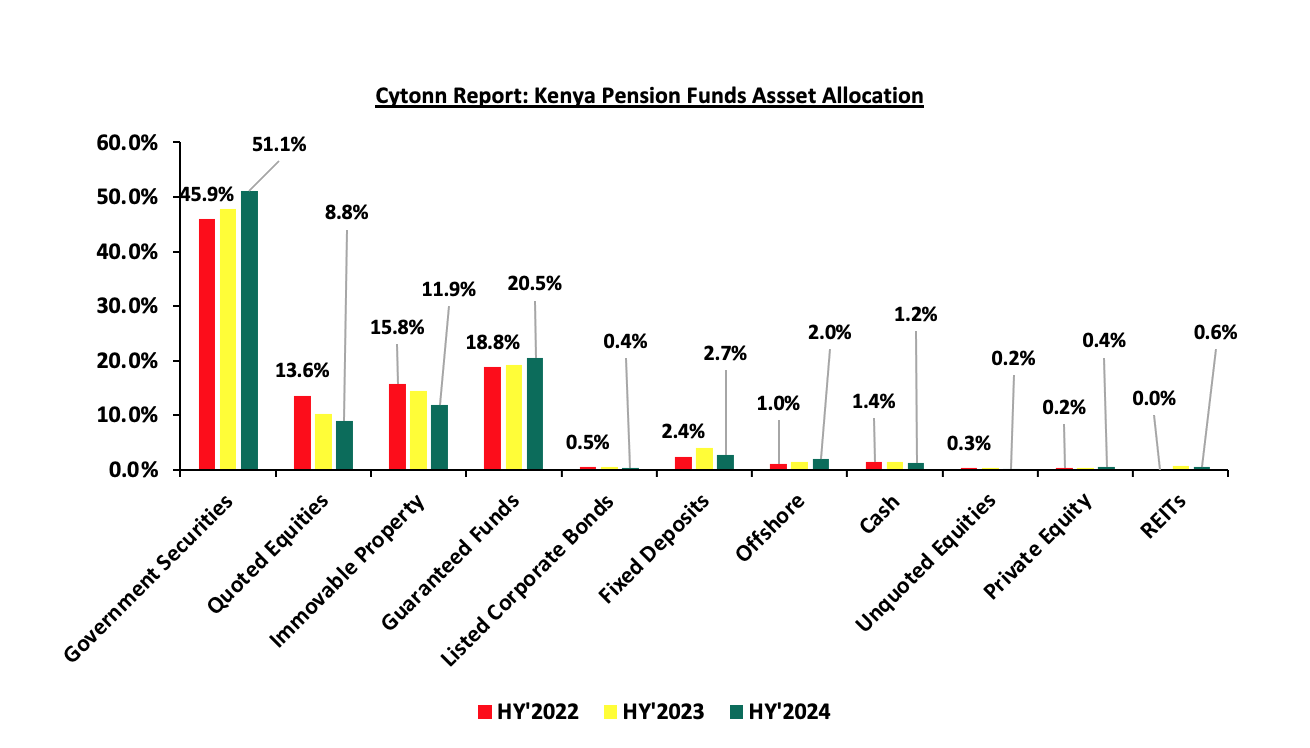

Retirement benefits schemes have for a long time skewed their investments towards traditional assets, mostly, government securities and the equities market, averaging 57.8% as of 30th June 2024 for the two asset classes, leaving only 42.2% for the other asset classes. However, as pension schemes seek higher returns, diversification, and inflation hedging, there has been a growing shift towards alternative investments that include immovable property, private equity as well as Real Estate Investments Trusts (REITs). It is vital to note, that in HY’2024 the second largest increase in allocation was recorded in investments in private equity by 63.3% to Kshs 8.8 bn from Kshs 5.4 bn recorded in HY’2023 and investments in Real Estate Investments Trusts increased by 4.5% to Kshs 11.1 bn in HY’2024 from Kshs 10.6 bn in HY’2023. However, allocation to immovable property decreased by 4.1% to Kshs 236.3 bn in HY’2024 from Kshs 246.3 bn in HY’2023.

Key Take-outs from the table above are;

- Schemes in Kenya allocated an average of 57.8% of their members’ funds towards government securities and Quoted Equities between the period of 2013 and end of June 2024. The 41.1% average allocation to government securities is the highest among the asset classes attributable to safety assurances of members’ funds because of low-risk associated with government securities. Notably, allocation towards government securities increased by 3.6% points to 51.1% in HY’2024 from 47.5% in FY’2023 attributable to high yields by the government papers and increased issuance of treasury bonds to finance fiscal deficits as well as increase domestic borrowing during the period,

- The allocation towards quoted equities increased to 8.8% as of June 2024, from 8.4% in December 2023 on the back of improved performance in the Kenyan equities market as evidenced by 19.0% of the NASI index in H1’2024, driven by a recovery in corporate earnings and increased investor confidence. Favourable macroeconomic conditions, such as easing inflation and a strengthened shilling, boosted market sentiment, have encouraged trustees to allocate more funds to equities during the period,

- Retirement Benefits Schemes investments in offshore markets increased by 0.4% points to 2.0% as of June 2024, from 1.6% in December 2023 as a result of the opportunities in developed and emerging markets, and currency hedging strategies that allowed schemes to benefit from foreign exchange gains, and,

- The 0.2% points increase in investment in commercial paper, non-listed bonds issued by private companies was due to an investment of Kshs 3.0 bn in Linzi sukuk bond by one of the schemes during the period.

The chart below shows the allocation by pension schemes on the three major asset classes over the years:

Source: RBA Industry report

- Performance of the Retirement Benefit Schemes

According to the ACTSERV Q4’2024 Pension Schemes Investments Performance Survey, the five-year average return for segregated schemes over the period 2020 to 2024 was 4.5% with the performance fluctuating over the years to a high of 13.2% in 2024 and a low of 0.7% in 2021 reflective of the markets performance. Notably, segregated retirement benefits scheme returns increased to a 13.2% return in Q4’2024, up from the 3.1% gain recorded in Q4’2023. The y/y growth in overall returns was largely driven by the 18.7% points increase in returns from Equities to 15.7% from a loss of 3.0% in Q4’2023 attributable to the increased corporate earnings and attractive valuations as well as the 13.3% gain from fixed income. The performance was however weighed down by the 17.2% points decline in the Offshore returns to 0.8%, from 18.0% in Q4’2023 majorly attributable to the uncertainty about the US general election and China’s weak economic data. The chart below shows the performance of segregated pension schemes since 2015:

Source: ACTSERV Survey Reports (Segregated Schemes), computed for quarters ending 31st December

The key take-outs from the graph include:

- Schemes recorded a 13.2% gain in Q4’2024, representing 12.8% points increase from the 0.4% gain recorded in Q3’2024. The performance was largely driven by the 15.7% returns from Equities attributable to the increased corporate earnings and attractive valuations as well as the 13.3% gain from fixed income. The performance was however weighed down by the 3.9% points decline in the Offshore returns to 0.8%, from 4.7% in Q3’2024 majorly attributable to the uncertainty about the US general election and China’s weak economic data, and,

- Returns from segregated retirement funds have exhibited significant fluctuations, ranging from a high of 13.2% recorded in Q4’2024 to a low of 0.7% in Q4’2021, highlighting the sensitivity of fund performance to market and economic conditions.

The survey covered the performance of asset classes in three broad categories: Fixed Income, Equity, Offshore, and Overall Return.

Below is a table showing the fourth quarter performances over the period 2020-2024:

|

Cytonn Report: Quarterly Performance of Asset Classes (2020 – 2024) |

|||||||

|

|

Q4'2020 |

Q4'2021 |

Q4'2022 |

Q4’2023 (a) |

Q4'2024 (b) |

Average (2020-2024) |

% points change (b-a) |

|

Equity |

5.9% |

(4.4%) |

(0.2%) |

(3.0%) |

15.7% |

2.8% |

18.7% |

|

Fixed Income |

2.0% |

2.2% |

2.9% |

4.0% |

13.3% |

4.9% |

9.3% |

|

Offshore |

8.5% |

7.2% |

7.4% |

18.0% |

0.8% |

8.4% |

(17.2%) |

|

Overall Return |

3.0% |

0.7% |

2.3% |

3.1% |

13.2% |

4.5% |

|

Source: ACTSERV Surveys

Key take-outs from the table above include;

- Returns from Equity investments recorded a significant increase by 18.7% points to a 15.7% gain in Q4’2024, from the 3.0% loss recorded in Q4’2023, driven by strong corporate earnings, attractive stock valuations and the the performance of the Kenyan currency in 2024, having gained by 17.4%, to close the year at Kshs 129.3 from the Kshs 157.0 recorded at the beginning of 2024, which boosted investor confidence. Additionally, declining bond yields made bonds less appealing, prompting investors to shift their focus to equities, further supporting market gains,

- Returns from Fixed Income also recorded an increase of 9.3% points to 13.3% in Q4’2024 from 4.0% recorded in Q4’2023. This performance in Q4’2024 is partially attributable to improved market conditions compared to a similar period in 2023, as evidenced by the higher yields on government securities and improved investor sentiment towards government debt instruments as well as an ease in inflationary pressures with the average inflation rate for Q4’2024 coming in at 2.8% from in 6.8% Q4’2023, and,

- Returns from the Offshore investments recorded a significant decrease to a 0.8% return in Q4’2024 from the 18.0% recorded in Q4’2023. The performance was partly attributable to the uncertainty surrounding the US general election introducing market volatility, limiting the gains that segregated schemes could achieve from their offshore allocations.

Other Asset Classes that Retirement Benefit Schemes Can Leverage on

- Alternative Investments (Immovable Property, Private Equity and REITs)

Retirement benefits schemes have for a long time skewed their investments towards traditional assets, mostly, government securities and the equities market, averaging at 57.8% in 10 years, as of 30th June 2024, leaving only 42.2% for all the other asset classes. In the asset allocation, alternative investments that include immovable property, private equity as well as Real Estate Investments Trusts (REITs) account for an average of only 17.5% against the total allowable limit of 70.0%. In terms of overall asset allocation, alternative investments still lagged way behind the other asset classes, as demonstrated in the graph below;

Source: RBA Industry Report

Alternative Investments refers to investments that are supplemental strategies to traditional long-only positions in equities, bonds, and cash. They differ from traditional investments on the basis of complexity, liquidity, and regulations and can invest in immovable property, private equity, and Real Estate Investment Trusts (REITs) to a limit of 70.0% exposure. We believe that Alternative Investments, including REITs, would play a significant role in improving the performance of retirement benefits schemes by providing opportunities for higher returns and enhanced portfolio resilience.

Alternative Investments, such as immovable property, private equity, and REITs, offer not only diversification and competitive long-term returns but also the potential to hedge against inflation. Investments in real assets like immovable property and REITs often benefit from inflationary environments, as property values and rental incomes tend to rise with inflation. Additionally, private equity provides access to high-growth sectors, such as technology and renewable energy, which are less correlated to traditional market movements, offering an attractive risk-adjusted return profile.

Furthermore, REITs in Kenya, particularly Development and Income REITs, present unique opportunities for retirement schemes. They provide exposure to the real estate sector without the liquidity constraints and management challenges associated with direct property ownership. As the Kenyan real estate market continues to mature and regulatory frameworks for REITs improve, these instruments are becoming more viable for retirement funds seeking stable, inflation-protected income streams and long-term growth. By strategically allocating a portion of their portfolio to alternative investments, retirement schemes can enhance overall returns while safeguarding members' contributions against market volatility.

- Public Private Partnerships

According to the Retirement Benefits Authority Investment Regulations and Policies, pension schemes can invest up to 10.0% of their total assets under management in debt instruments for the financing of infrastructure or affordable housing projects approved under the Public Private Partnerships Act. Kenya's pension schemes are increasingly investing in infrastructure projects to diversify their portfolios, achieve stable long-term returns, and contribute to national development. A significant initiative in this direction is the Kenya Pension Funds Investment Consortium (KEPFIC), established in 2018. KEPFIC is a collective of prominent Kenyan retirement benefit funds that have united to make long-term investments in infrastructure and alternative assets within the region. As of the latest report, KEPFIC has mobilized over USD 113.0 mn into projects such as roads, student housing, and affordable housing, involving 88 local pension funds.

Despite there being 1,075 registered pension schemes in Kenya, only 88 have actively participated in infrastructure investments through KEPFIC, highlighting a significant untapped opportunity. With the Retirement Benefits Authority allowing schemes to allocate up to 10.0% of their assets into such projects, there remains substantial room for more pension funds to diversify into infrastructure and affordable housing. A prime example of this opportunity is the Usahihi Expressway, a 440-kilometer dual carriageway connecting Nairobi and Mombasa, which seeks to raise approximately USD 1.0 bn from local pension funds and financial institutions as part of its estimated USD 3.5 bn cost. The Usahihi Expressway is expected to generate revenue primarily through toll collections over the 30-year concession period. Toll roads historically provide stable, inflation-hedged cash flows, making them attractive to long-term institutional investors like pension funds. Toll roads generate cash flows that grow over time, as toll rates can be adjusted for inflation and traffic volumes are expected to increase. By participating in this Public-Private Partnership, pension schemes can not only enhance portfolio returns and manage long-term risks but also play a crucial role in national development by financing transformative projects that spur economic growth.

Section III: Factors Influencing the Growth of Retirement Benefit Schemes

The retirement benefit scheme industry in Kenya has registered significant growth in the past 10 years with assets under management growing at a CAGR of 9.4% to Kshs 1.7 tn in FY’2023, from Kshs 0.7 tn in FY’2013. The growth is attributable to:

- Legislation – The National Assembly, on 26th December 2024, assented to the Tax Laws (Amendment) Bill 2024. The Bill amended the Income Tax Act by increasing the deductible amount for contributions to registered pension, provident, and individual retirement funds or public pension schemes to Kshs 360,000 annually from Kshs 240,000 and introduced provisions that allow contributions to post-retirement medical funds up to Kshs 15,000 per month—to be tax-deductible. Additionally, income from registered retirement benefits schemes is now tax-exempt for individuals who have reached the retirement age set by their scheme, those withdrawing benefits early due to ill health, or those exiting a registered scheme after at least 20 years of membership. These changes aim to adjust for inflation and modernize deductions that have remained unchanged for over a decade. The revisions are expected to reduce individual taxable income and enhance retirement benefits. In addition, the implementation of the National Social Security Fund Act, 2013 is entering its third year and is expected to foster the growth of the pension industry by allowing both the employees in the formal and informal sector to save towards their retirement. The upward revision of the NSSF Tier 1 and Tier 2 contribution limits effective from February 2025, to Kshs 8,000 and 72,000 respectively from Kshs 7,000 and Kshs 36,000 respectively is expected to enhance retirement savings, improving pension adequacy for retirees,

- Public-Private partnerships - Public-private partnerships can be instrumental in expanding financial inclusion in the Kenyan pension sector. Collaborations between the government and private financial institutions can lead to the development and promotion of inclusive pension products. In Kenya, the National Social Security Fund (NSSF) is currently licensing and partnering with the private sector (Pension Fund Managers) to invest and manage NSSF Tier II contributions. This is a good example that the government is giving employees, employers, and persons in the informal sector to invest and save for their retirement in the private sector,

- Increased Pension Awareness – More people are becoming increasingly aware of the importance of pension schemes and as such, they are joining schemes to grow their retirement pot which they will use during their golden years. Over the last 20 years, pension coverage has grown from 12.0% to about 26.0% of the labour force. The Retirement Benefits Authority, through their Strategic Plan 2024-2029, aims to further expand this coverage to 34.0% by 2029. This growth reflects industry-wide initiatives to increase awareness among Kenyan citizens on the need for retirement planning and innovations,

- Tax Incentives - Members of Retirement Benefit Schemes are entitled to a maximum tax-free contribution of Kshs 30,000 monthly. Consequently, pension scheme members enjoy a reduction in their taxable income and pay less taxes. This incentive has motivated more people to not only register but also increase their regular contributions to pension schemes,

- Micro-pension schemes - Micro-pension schemes are tailored to address the needs of Kenyans in the informal sector with irregular earnings. These schemes allow people to make small, flexible contributions towards their retirement. By accommodating their financial realities, micro-pensions can attract a broader segment of the population into the pension sector. Examples of these pension schemes are Mbao Pension Plan and Individual Pension Schemes where one can start saving voluntarily and any amount towards their retirement,

- Relevant Product Development – Pension schemes are not only targeting people in formal employment but also those in informal employment through individual pension schemes, with the main aim of improving pension coverage in Kenya. To achieve this, most Individual schemes have come up with flexible plans that fit various individuals in terms of affordability and convenience. Additionally, the National Social Security Fund Act, 2013 contains a provision for self-employed members to register as members of the fund, with the minimum aggregate contribution in a year being Kshs 4,800 with the flexibility of making the contribution by paying directly to their designated offices or through mobile money or any other electronics transfers specified by the board,

- Technological Advancement – The adoption of technology into pension schemes has improved the efficiency and management of pension schemes. A notable example of pension technology in Kenya is the M-Akiba platform. This is a mobile-based platform that was developed by the government to enable Kenyans to save for their retirement using their mobile phones. Additionally, the improvement of mobile penetration rate and internet connectivity has enabled members to make contributions and track their benefits from the convenience of their mobile phones, and,

- Financial literacy programs - Financial literacy programs play a vital role in promoting the growth of retirement benefit schemes by enhancing financial inclusion among the public. Educating the public about the benefits of retirement savings and how to navigate pension schemes can empower individuals to take control of their financial future. The Retirement Benefits Authority (RBA) is at the forefront of ensuring the public is educated on financial literacy by organizing free training.

Section IV: Challenges that Have Hindered the Growth of Retirement Benefit Schemes

Although the Retirement Benefit industry is expanding, several obstacles still hinder its progress. The main challenges include:

- Low Pension Coverage in the Informal Sector – Many informal sector workers and small businesses lack access to structured retirement savings plans, leaving a significant portion of the Kenya’s workforce without adequate retirement security due to irregular incomes and job insecurity. The Retirement Benefit Statistical Digest 2021 reports that only 266,764 individuals are registered in individual pension schemes. This number is low compared to the 15.2 mn people in the informal sector, representing 83.2% of the total workforce (Kenya National Bureau of Statistics Economic Survey Report 2023). Many individuals in this sector focus on immediate financial needs rather than long-term savings, and traditional pension products may not align with their financial circumstances,

- Market Volatility – In segregated schemes, investment returns are not assured and fluctuate with market conditions. In Q4’2024 the equities market registered an increase of 15.7% a reversal from decline by 2.2% in Q3’2024, following a 3.2% drop in Q2’2024, coming after a significant 22.8% gain in Q1 2024. This volatility creates uncertainty in the growth of retirement savings.

- Low Awareness and Financial Literacy- Lack of awareness and understanding of retirement planning among individuals reduces participation rates, leading to inadequate savings for retirement. Many individuals don't fully understand the importance of saving for retirement or the lasting benefits of participating in a pension plan. This lack of understanding often originate from not being aware of these options, the advantages they offer, or how to enrol. This issue is particularly common in rural or underserved areas, where access to information is limited,

- Inadequate Contributions - Even when individuals are covered by retirement schemes, their contributions are often inadequate to meet future financial needs due to factors such as low disposable income, delayed enrolment in schemes and inadequate contribution rates. Insufficient contributions translate directly into lower payouts upon retirement. For retirees, this can result in financial insecurity, dependence on family or government assistance and inability to meet basic living expenses,

- High Level of Unemployment – According to the Kenya National Bureau of Statistics Q4’2022 labour report, 6% of Kenya’s 29.1 mn working-age population aged between 15-64 years was unemployed. The high unemployment rate presents a major obstacle for many individuals, preventing them from making consistent contributions to retirement schemes,

- Premature Access to Savings – Members of individual pension schemes can withdraw 100.0% of their own contributions, though this does not include any employer contributions that have been transferred. On the other hand, members in umbrella and occupational schemes can access up to 50.0% of their accumulated benefits before reaching retirement age, typically in situations such as job loss or a change in employment. In recent developments made a proposal to stop workers from accessing the pension savings in order to help retirees have adequate savings after their retirement. The regulator wants to remove the part of the law that allows workers under the age of 50 to access half of their of their pensions benefits when they switch jobs. While this new proposal does not offer immediate financial relief, it increases the overall value of retirement savings, thereby encouraging the pension sector's long-term growth potential.

- Unremitted Contributions – Due to financial constraints, some employers have postponed or failed to remit pension contributions to umbrella and occupational schemes. As a result, unremitted contributions have increased significantly, growing to Kshs 61.8 billion in 2023 from Kshs 42.8 billion in 2022 according to the Retirement Benefits Statistical Digest 2023, and,

- Delayed Benefit Payments –Streamline the approval process by cutting down on the number of steps and parties involved. Pension scheme administrators should have greater autonomy in calculating and approving payments, which would help speed up disbursements. Additionally, implementing automated systems to calculate and process benefits can minimize manual work and reduce the time spent transferring files between service providers.

Section V: Recommendations to Enhance the Growth and Penetration of Retirement Benefit Schemes in Kenya

- Increase Public Education and Awareness – Initiate targeted campaigns to inform the public about the importance of planning for retirement and the benefits of pension schemes. Organize workshops and seminars in rural and underserved communities to simplify pension concepts and boost understanding in terms of how to join, benefits of joining and process of exiting. The Retirement Benefits Authority (RBA) has recently been leading this essential campaign by hosting seminars, workshops, and roadshows to achieve these goals.

- Improve Regulatory Framework to Address Unremitted Contributions – The Retirement Benefits Authority (RBA) should enhance its oversight of employers to ensure pension contributions are fully and promptly remitted. Non-compliant employers should be subject to stricter penalties, such as fines or legal action, to encourage timely payments. However, for businesses experiencing short-term financial difficulties, RBA could provide options for structured payment plans or deadline extensions, helping them meet their obligations without defaulting. Additionally, RBA could involve Kenya Revenue Authority (KRA) to collect unremitted pension contributions and remit to RBA. KRA shall issue agency notices requiring holders of unremitted pension contributions to pay up within a specified date or notify KRA of their inability to pay due to lack of funds within 14 days of the receipt of the notice.

- Introduce Policy Reforms to Limit Premature Withdrawals – To safeguard long-term retirement savings, the percentage of pension funds accessible before retirement should be further reduced. Withdrawals should only be permitted in cases of genuine emergencies, such as critical illness, and must be supported by clear documentation and justification. Additionally, retirement schemes should provide educational workshops and materials to raise awareness about the long-term benefits of sustained savings and the financial risks associated with early withdrawals.

- Develop Tailored Pension Products for the Informal Sector – RBA should explore ways of encouraging the development of products with low, flexible contribution thresholds aimed at reaching the informal sector with irregular contributions. Targeting this section would greatly improve the pension coverage in the country. Leverage mobile money platforms and apps to facilitate seamless enrolment, contributions, and tracking of pension accounts.

- Promote Employees and Employer Participation in Pension Schemes – The Retirement Benefits Authority (RBA) should introduce incentives to encourage higher pension savings. This could include enhanced tax benefits for individuals and employers who contribute more to their pension schemes or a matching contribution system for voluntary savings. Such measures would motivate employees and employers to save beyond the mandatory contributions, ultimately improving retirement security and financial well-being.

- Streamline the Benefit Payment Process – The approval and disbursement of retirement benefits should be streamlined to minimize delays. Implementing automation for key processes and establishing clear timelines for each stage would ensure that retirees receive their benefits promptly. This efficiency would enhance trust in pension schemes and encourage greater participation, ultimately strengthening the retirement savings culture.

Implementing these recommendations will play important role in driving the sustainable growth of Kenya's retirement benefit schemes. By tackling key structural challenges faced in the industry, it will lead to enhanced trust, increased participation, and ultimately strengthen the sector’s long-term impact.

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is following Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice, or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.